Written by Andy Cave, IMEC Regional Manager

An example of how an accounting approach may hinder continuous improvement efforts

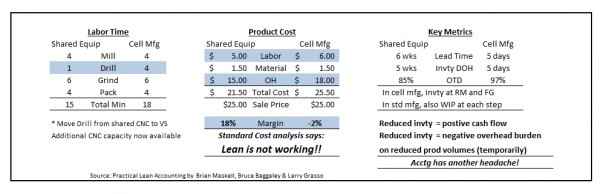

The Accounting concept of Standard Costing was developed in the 1920’s, and its application has remained fairly constant. Manufacturing was noted for minimal product variation (“You can buy a Model T in any color, as long as it’s black”) and long production runs creating lots of inventory whose financial value had to be estimated. Lean principles have changed the manufacturing world significantly, with shorter set-up times and significantly less inventory. Meanwhile, Accounting still spends time analyzing and understanding labor, material and overhead variances; often generating thousands of related transactions and accrual entries. In the Lean world, these are Non Value-Added activities; the customer is not willing to pay more for our cost variance analysis excellence.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}